+91 6002993949

submission@himjournals.com

Open Access

ISSN (Print) : 2709-3549

ISSN (Online) : 2709-3557

In this study trying to estimate volatility of returns of Dhaka stock exchange and compare volatility of overall periods and financial crises periods and trying to find out the best fitted model for DSE30 companies between two periods using symmetric GARCH model and asymmetric GARCH model. Time series analysis especially symmetric and asymmetric GARCH model has been conducted to estimate volatility, to find best fitted model and lastly comparing the results of DSE30 companies between two periods. After analysis finally results show that volatility for financial crisis period specially IDLC Finance Limited, IFAD Autos Limited, Pubali Bank Limited, The ACME Laboratories companies are extremely high and un stationary comparative to overall periods. So according to result say that DSE30 companies of financial crisis periods produces instability in the capital market, destabilizes the value of currency, as well as hampers international trade and finance.

Volatility is basically a function of uncertainty."-say‘s John Bollinger. In order to prevent uncertainty and risk in the stock market, it is particularly important to measure effectively the volatility of stock index returns. It measures the difference between an asset current prices and its average past prices. It can also be measured by using the standard deviation or variance between returns from the same security or market index. The standard deviation tells us how tightly the price of a stock is grouped around the mean or moving average. When the prices are tightly bunched together, the standard deviation is small. When the price is spread apart, you have a relatively large standard deviation. Volatility tends to decline as the stock market rises and increases as the stock market falls. When volatility increases, risk increases and returns decrease. If there is a wide range of fluctuations in the prices over short time periods, it has high volatility and has low volatility if the price moves slowly. Greater volatility influences risk adverse investors to demand a higher risk premium. High indices of the stock market in every aspect of measurement implied less variability of volatility. The extreme volatility in the stock market produces instability in the capital market, destabilizes the value of currency, as well as hampers international trade and finance. Usually due to financial crises, stock market volatility rises very high due to a heavy drop in stock prices across global markets; with the effects on the emerging markets remaining heavy and persistent. At the same time, financial market volatility has also a direct impact on macroeconomic and financial stability. In this study two periods are counted that are overall periods (up to 2020) and financial crises period (2020) due to the corona crisis. It is the case study of Dhaka Stock Exchange of Bangladesh. The comparative study of this research is to estimate the volatility modeling of these two periods. In the previous volatility related area different things are estimated on volatility modeling which are presented in literature review. But in this research comparative study between two periods is done using DSE data. To complete the research different statistical analysis specifically time series analysis are used. As a result volatility modeling expresses the financial condition of DSE of Bangladesh.

The main objectives of this study are given:

To estimate volatility of the returns of Dhaka stock exchange

To Compare volatility between overall periods and financial crises periods

To find out the best fitted model for DSE between symmetric GARCH model and asymmetric GARCH model

Literature review: Banamber et al. [1] presented that the stock market returns of India are more predictable based on the lagged-realized rates of return and less efficient than those of Japan and evidence of volatility persistence in both markets. The estimates of the mean-model show ARCH-components in the rates of stock market return in India while that is not the case for Japan. They indicate that the stock market of Japan is relatively more efficient than that of India. There are evidences of asymmetric effects of bad news and good news on stock market returns of India and Japan. Apparently, India's stock market is influenced more by positive news and Japan's stock market is influenced more by negative news. There is also evidence of volatility persistence in both markets. Debesh et al. [2] studied various dimensions of stock market volatility including measurement and nature of impact of volatility with the help of important economic literatures. It emphasized also on the political factors of volatility and attempted to relate economic growth with stock market volatility in the long run process reviewing a few econometric models and concludes that political instability and depression catapulted the stock market volatility which dwindled the growth rate of a country including a strong negative spillover effects of volatility from other countries on growth rate .The nexus between international trade and volatility was explained through econometric models showing asymmetric in nature where volatility reduces both volume of trade and increases current account and capital account deficits.

Mamtha et al. [3] intended to understand the characteristics of volatility and provides the insight of cause and effect of volatility of stock prices and also attempts to bring out various features of volatility such as volatility clustering, mean reversion and degree of volatility persistence. They found that factors like information flow, trading volume, economical aspects and investor’s behavior are the causes of volatility in the stock market. It also suggests that the stock markets around the world have evidenced asymmetry response and spillover effects of volatility.

Maqsood et al. [4] estimated that stock returns volatility for the Kenya’s Nairobi Securities Exchange (NSE), by applying different univariate specifications of GARCH type models. The results show that the volatility process is highly persistent, thus, giving evidence of the existence of risk premium for the NSE index return series. This in turn supports the positive correlation hypothesis: that is between volatility and expected stock returns. Another fact revealed by the results is that the asymmetric GARCH models provide better fit for NSE than the symmetric models. This proves the presence of leverage effect in the NSE return series.

Raheem et al. [5] showed that considering all the bank returns are highly leptokurtic, significantly skewed and thus non-normal across the four periods except for Fidelity bank during financial crises; find-ings similar to those of other global markets. The global financial market had significant impacts on the stock returns Due to the higher rates of persistence in volatility during the financial crisis across the 10 banks than they were at the overall period, is an indication that the banks became riskier due to the crisis. Asymmetric GARCH models outperformed the symmetric GARCH models, especially during the financial crises and post the crises. They also conclude that Nigerian banks’ returns are volatility persistent during and after the crises, and are characterized by leverage effects of negative and positive shocks during these periods.

Roni et al. [6] examine that the effective GARCH models recommended for performing market returns and volatilities analysis, to conduct a content analysis of return and volatility literature, to observe studies which use directional prediction accuracy model as a yardstick from a realistic point of understanding and has the core objective of the forecast of financial time series in stock market return and presents a comprehensive literature which has mainly focused on studies on return and volatility of stock market using systematic review methods on various financial markets around the world.

Sartaj et al. [7] presented that volatility on a daily basis has been found to have clustering patterns and important for the markets as it signals about their health, what is not desirable is erratic behavior of volatility taking an extreme form.

The data will be collected from Dhaka stock exchange consisting of daily closing stock prices which covers overall periods and financial crises periods. At first calculate return of each company between two periods and then descriptive statistics has been analyzed. The return is calculated using the given formula:

Rt ![]()

where, PT is the stock price at time t and ![]() is the stock price at time t-1.

is the stock price at time t-1.

Time series analysis specially symmetric and asymmetric GARCH model has been conducted of return data of each company between two periods. The Autoregressive Conditional Heteroscedastic (ARCH) family models are adopted in modeling financial data for a number of reasons which include simplicity and ease of ability to handle clustered errors and changes in the econometricians’ leverage to make predictions.

Autoregressive Conditional Heteroscedasticity (ARCH) and Generalized Autoregressive Conditional Heteroscedasticity (GARCH): For ARCH (1) the conditional volatility is ![]() =

=![]() +

+![]() , will be positive and stationary if

, will be positive and stationary if ![]() and

and![]() . The unconditional volatility for ARCH (1) is

. The unconditional volatility for ARCH (1) is ![]() =

=![]() , where

, where ![]() is the long run volatility and

is the long run volatility and ![]() is the coefficient of heteroscedasticity or measures ARCH effect. It means it seems that there is a volatility clustering because high changes mean high fluctuations and low changes means low fluctuations. ARCH LM-test; Null hypothesis: no ARCH effects. When p value is less than 5% or 1% we can easily say that there is ARCH effect. So it said that there are no ARCH effects. Then GARCH model, EGARCH model and TGARCH model are applied in each company and choose best mode based on Akaike Information Criteria(AIC) because we know that the least value of AIC is known as the best model. The persistence to volatility is however determined by

is the coefficient of heteroscedasticity or measures ARCH effect. It means it seems that there is a volatility clustering because high changes mean high fluctuations and low changes means low fluctuations. ARCH LM-test; Null hypothesis: no ARCH effects. When p value is less than 5% or 1% we can easily say that there is ARCH effect. So it said that there are no ARCH effects. Then GARCH model, EGARCH model and TGARCH model are applied in each company and choose best mode based on Akaike Information Criteria(AIC) because we know that the least value of AIC is known as the best model. The persistence to volatility is however determined by![]()

![]() .

.

Exponential Autoregressive Conditional Heteroscedasticity (EGARCH): For EGARCH(1,1) the conditional volatility is:

ln(![]() ) =

) = ![]() +

+![]() (

(![]() )+

)+![]() ln(

ln(![]() )+δ

)+δ![]() )- E

)- E![]() )

)

where, δ is the leverage parameter that would be computed along with ![]() and

and![]() . Above Equation has in its last term the difference between absolute residuals and its expectation which produces leverage effects (effects which dis-tinguishes the impacts of positive shocks from negative shocks to the stock re-turns). EGARCH is however unrestricted in the course of model estimation because with the natural log of, the volatility equation will always be positive. The persistence to volatility is however determined by

. Above Equation has in its last term the difference between absolute residuals and its expectation which produces leverage effects (effects which dis-tinguishes the impacts of positive shocks from negative shocks to the stock re-turns). EGARCH is however unrestricted in the course of model estimation because with the natural log of, the volatility equation will always be positive. The persistence to volatility is however determined by ![]() . Leverage effect means negative correlation between past return and volatility of future return. In order to apply EGARCHrequire the coefficients of gamma is negative and significant but gamma is positive so there is no Leverage effect. If there is no Leverage effect cannot go for EGARCH.

. Leverage effect means negative correlation between past return and volatility of future return. In order to apply EGARCHrequire the coefficients of gamma is negative and significant but gamma is positive so there is no Leverage effect. If there is no Leverage effect cannot go for EGARCH.

Threshold Autoregressive Conditional Heteroscedasticity (TGARCH): It helps to compute asymmetries in terms of negative and positive shocks. It simply means this model treats good news and bad news asymmetrically:

![]() =Ꙍ+α

=Ꙍ+α![]() +β

+β![]() +γ

+γ![]()

where, ![]() = 1, bad news, 0 otherwise. Good news related with positive shock, has impact of beta whereas bad news has an impact of beta and gamma. γ>0 indiicates asymmetry or leverage effect but γ = 0 symmetry in volatility. If (α+γ) >=0 and γ<0, it means the model will be good. The shock persistence is measured by:

= 1, bad news, 0 otherwise. Good news related with positive shock, has impact of beta whereas bad news has an impact of beta and gamma. γ>0 indiicates asymmetry or leverage effect but γ = 0 symmetry in volatility. If (α+γ) >=0 and γ<0, it means the model will be good. The shock persistence is measured by:

![]()

![]() +

+ ![]() .

.

Relative persistence of volatility: Trying to compute relative volatility persistence (RP) of the financial crisis period relative to the overall periods to determine what proportion of the overall persistence in volatility was accounted for during the crisis. This would enable us to understand level of risk that was recorded by each company during the period. Suppose that the persistence in volatility during the crisis and at the overall period is respectively defined as ![]() and

and![]() , the relative persistence in volatility during the crisis is then defined mathematically as:

, the relative persistence in volatility during the crisis is then defined mathematically as:

![]() =

= ![]()

Descriptive statistics: In this section summary statistics of DSE30 companies for the Covid-19 Periods and Non Covid-19 Periods are presented by considering Covid-19 Periods as a financial crisis periods and Non Covid-19 Periods as overall periods.

Table 1 and 2 represent the summary statistics of DSE30 companies between financial crisis periods and overall periods. Observing that mean returns of DSE30 companies are not zero between two periods except singer Bangladesh Ltd. of Covid-19 period while median of Covid-19 period are all about zero but with regards to overall periods medians are non-zero except Eastern Bank Ltd., National Bank Ltd., Pubali Bank Ltd. And Summit power Ltd. The standard deviations of covid-19 period are higher than overall periods indicating high variability around the mean across DSE30 companies.

To test the suitability of ARCH or GARCH family models, ARCH (1), GARCH (1,1), EGARCH (1,1) and

TGARCH(1,1) models are fitted to the returns of each companies and the Akaike Information Criterion (AIC) obtained for each period considered. The appropriate model is chosen by considering the least AIC results of which are provided in Table 3. From Table 3, clear to us that there is no DSE30 companies are fitted with ARCH(1), only Beximco Pharmaceuticals Ltd. is fitted with GARCH(1,1) and remaining 21 companies i.e. Bangladesh Export Import Co., Bangladesh Steel Re-Rolling, Bangladesh Submarine Cab Co., Beacon Pharmaceuticals Ltd., BRAC Bank Ltd., British American Tobacco Bangladesh Co., Confidence Cement Ltd., Eastern Bank Ltd., Grameenphone Ltd., IFAD Autos Limited, Lafarge Holcim Bangladesh, Lanka Bangla Finance Ltd., Olympic Industries Limited, Padma Oil Co.Ltd., Paramount Textile Limited, Renata Ltd., Singer Bangladesh Ltd., Square Pharmaceuticals Ltd., Summit Power Ltd., Titas Gas Trans. & Dist. Co., United Power Generation companies are fitted with EGARCH(1,1) and also remaining 9 companies i.e BBS Cables Limited, City Bank Ltd., IDLC Finance Limited, Meghna Petroleum Ltd., National Bank Ltd., National Life Insurance Co., Pubali Bank Ltd., The ACME Laboratories are fitted with TGARCH(1,1) models.

The volatility persistence of IDLC Finance Limited, IFAD Autos Limited, Pubali Bank Limited, The ACME Laboratories companies are extremely high and un stationary. So according to result say that DSE30 companies of financial crisis periods produces instability in the capital market, destabilizes the value of currency, as well as hampers international trade and finance.

To test the suitability of ARCH or GARCH family models, ARCH (1), GARCH (1,1), EGARCH (1,1) and TGARCH (1,1) models are fitted to the returns of each companies and the Akaike Information Criterion (AIC) obtained for each period considered. The appropriate model is chosen by considering the least AIC results of which are provided in Table 4. From Table 4, clear to us that there is no DSE30 companies are fitted with ARCH (1) and 8 companies such as Bangladesh Steel Re-Rolling, Beximco Pharmaceuticals Ltd., BRAC Bank Ltd., British American Tobacco Bangladesh Co., City Bank Ltd., IFAD Autos Limited, Lanka Bangla Finance Ltd, Olympic Industries Limited companies are fitted with GARCH(1,1) and 16 companies such as Bangladesh Export Import Co., BBS Cables Limited, Beacon Pharmaceuticals Ltd., Eastern Bank Ltd., Grameenphone Ltd., IDLC Finance Limited, Lanka Bangla Finance Ltd., Meghna Petroleum Ltd., Padma Oil Co.Ltd., Paramount Textile Limited, Renata Ltd., Singer Bangladesh Ltd., Summit Power Ltd., The ACME Laboratories, Titas Gas Trans. & Dist. Co., United Power Generation companies are fitted with EGARCH (1,1) and remaining 6 companies such as Bangladesh Submarine Cab Co., Confidence Cement Ltd., National Bank Ltd., National Life Insurance Co., Pubali Bank Ltd., Square Pharmaceuticals Ltd. companies are fitted with TGARCH(1,1) models.

Table 1: Summary Statistics of DSE30 Companies for the Covid-19 Periods: 22.03.2020-30.04.2021 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

Table 2: Summary Statistics of DSE30 Companies for the Non Covid-19 Periods: 30.04.2019-05.03.2020

SL No. | Name of companies | Mean | Median | Stdeviation | Skewness | Kurtosis |

1 | Bangladesh Export Import Co | 0.0022 | 0.0045 | 0.023 | -0.8687 | 2.7982 |

2 | Bangladesh Steel Re-Rolling | 0.0005 | 0.0016 | 0.023 | -0.1784 | 4.8834 |

3 | Bangladesh Submarine Cable Co. | 0.0026 | 0.0059 | 0.0259 | -0.6963 | 0.5873 |

4 | BBS Cables Limited | 0.0021 | 0.0011 | 0.0207 | -0.5427 | 2.0915 |

5 | Beacon Pharmaceuticals Ltd. | -0.0054 | -0.0022 | 0.0261 | -0.4722 | 1.2666 |

6 | Beximco Pharmaceuticals Ltd. | 0.0009 | 0.0012 | 0.0159 | -1.196 | 6.6452 |

7 | BRAC Bank Ltd. | 0.0025 | 0.0032 | 0.0216 | 0.454 | 4.9436 |

8 | British American Tobacco Bangladesh Co. | 0.0018 | 0.0035 | 0.0167 | -0.8607 | 3.1827 |

9 | City Bank Ltd. | 0.0019 | 0.0035 | 0.0198 | -0.5231 | 2.3115 |

10 | Confidence Cement Ltd. | 0.0022 | 0.0034 | 0.0236 | 1.2326 | 12.1703 |

11 | Eastern Bank Ltd. | 0.0011 | 0 | 0.0194 | 4.1881 | 40.2491 |

12 | Grameenphone Ltd. | 0.0017 | 0.0036 | 0.0218 | -0.906 | 3.7029 |

13 | IDLC Finance Limited | 0.0015 | 0.0008 | 0.0172 | -0.3999 | 2.0141 |

14 | IFAD Autos Limited | 0.0028 | 0.0045 | 0.0254 | -0.1516 | 1.1793 |

15 | LafargeHolcim Bangladesh | -0.0002 | 0.0025 | 0.0236 | -0.6273 | 2.6696 |

16 | LankaBangla Finance Ltd. | 0.0017 | 0.0056 | 0.0243 | -0.9935 | 2.1499 |

17 | Meghna Petroleum Ltd. | 0.0007 | 0.001 | 0.016 | -0.2694 | 7.0967 |

18 | National Bank Ltd. | 0.0011 | 0 | 0.019 | 0.4488 | 10.4441 |

19 | National Life Insurance Co. | -0.0013 | 0.0025 | 0.0278 | -0.8382 | 2.0529 |

20 | Olympic Industries Limited | 0.0014 | 0.0022 | 0.0188 | -0.0701 | 0.9173 |

21 | Padma Oil Co.Ltd. | 0.0015 | 0.0022 | 0.0174 | -0.1799 | 4.9511 |

22 | Paramount Textile Limited | 0.0005 | 0.0016 | 0.0202 | 0.0482 | 2.3253 |

23 | Pubali Bank Ltd. | 0.0007 | 0 | 0.0102 | -0.2281 | 2.7522 |

24 | Renata Ltd. | 0.0002 | 0.0005 | 0.0122 | 2.9311 | 22.5953 |

25 | Singer Bangladesh Ltd. | 6.85E-05 | 1.70E-03 | 1.56E-02 | 2.06E-01 | 2.11E+00 |

26 | Square Pharmaceuticals Ltd. | 0.0018 | 0.0008 | 0.0154 | 0.8653 | 17.3697 |

27 | Summit Power Ltd. | 0.0003 | 0 | 0.0135 | 1.2491 | 9.2924 |

28 | The ACME Laboratories | 0.0012 | 0.0014 | 0.0153 | -0.6058 | 1.2026 |

29 | Titas Gas Trans. & Dist. Co. | 0.0009 | 0.0027 | 0.0143 | -0.6915 | 11.2592 |

30 | United Power Generation | 0.0012 | 0.0021 | 0.0231 | 0.8924 | 8.4566 |

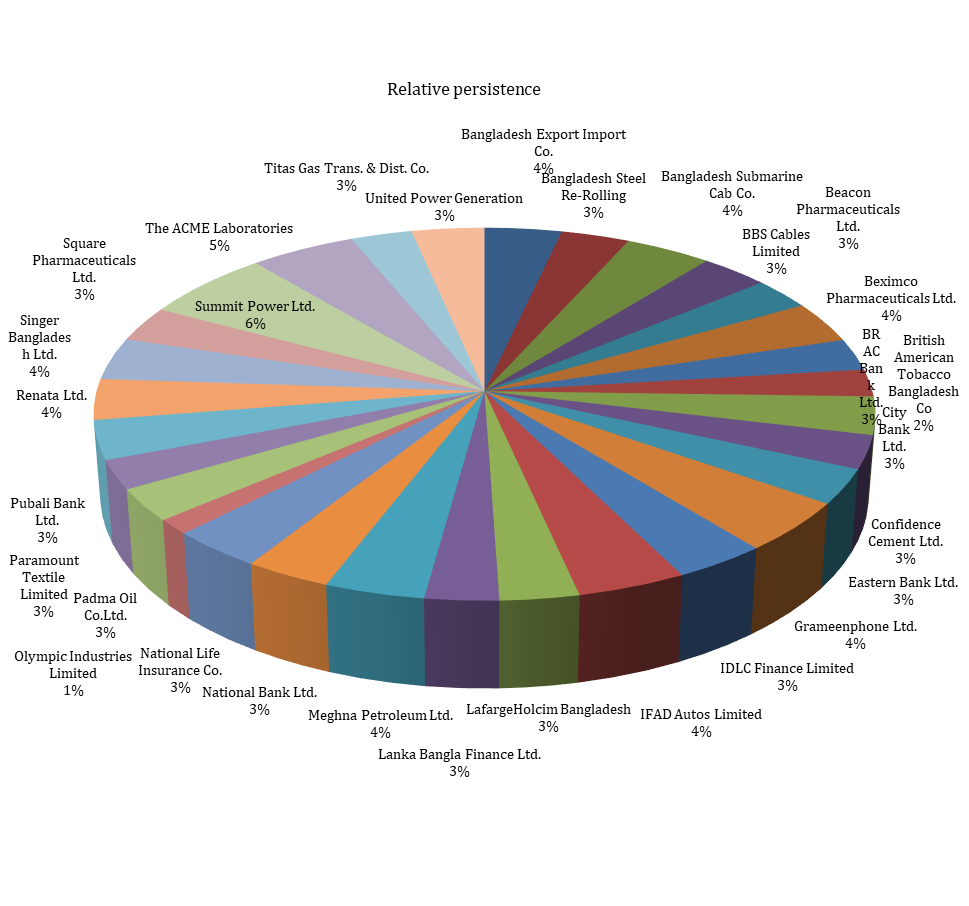

Fig. 1: Relative Persistence of financial crisis period to overall period

Table 3: Appropriate best fitted volatility model for DSE30 companies during Covid-19 Periods: 22.03.2020-30.04.2021

| Companies | Model | Persistence | ||||

| 1.Bangladesh Export Import Co. | EGARCH(1,1) | -0.489511 | 0.026719 | 0.918064 | 0.479570 | 0.918064 |

| 2. Bangladesh Steel Re-Rolling | EGARCH(1,1) | -0.412694 | 0.424390 | 0.932826 | 0.696518 | 0.932826 |

| 3.Bangladesh Submarine Cab Co. | EGARCH(1,1) | -0.875377 | 0.135115 | 0.868948 | 0.432348 | 0.868948 |

| 4.BBS Cables Limited | TGARCH(1,1) | 0.000095 | 0.863617 | 0.446402 | -0.811732 | 0.904153 |

| 5.Beacon Pharmaceuticals Ltd. | EGARCH(1,1) | -1.157342 | 0.068873 | 0.811059 | 0.904726 | 0.811059 |

| 6.Beximco Pharmaceuticals Ltd. | GARCH(1,1) | 0.000064 | 0.155998 | 0.805319 | N/A | 0.961317 |

| 7.BRAC Bank Ltd. | EGARCH(1,1) | -1.315046 | 0.202524 | 0.816544 | 1.207531 | 0.816544 |

| 8.British American Tobacco Bangladesh Co | EGARCH(1,1) | -2.14535 | -0.23818 | 0.69619 | 1.67262 | 0.69619 |

| 9.City Bank Ltd. | TGARCH(1,1) | 0.000087 | 0.508580 | 0.666952 | -0.434417 | 0.9583235 |

| 10.Confidence Cement Ltd. | EGARCH(1,1) | -1.064211 | 0.221852 | 0.855276 | 1.155212 | 0.855276 |

| 11.Eastern Bank Ltd. | EGARCH(1,1) | -0.857226 | 0.283117 | 0.884969 | 0.867658 | 0.884969 |

| 12.Grameenphone Ltd. | EGARCH(1,1) | -0.970983 | 0.014155 | 0.863294 | 1.939004 | 0.863294 |

| 13.IDLC Finance Limited | TGARCH(1,1) | 0.000000 | 0.474230 | 0.619259 | -0.188980 | 0.998999 |

| 14.IFAD Autos Limited | EGARCH(1,1) | -0.008027 | 0.370425 | 1.000000 | 0.404275 | 1.000000 |

| 15.LafargeHolcim Bangladesh | EGARCH(1,1) | -0.839839 | 0.270288 | 0.873628 | 0.693145 | 0.873628 |

| 16.Lanka Bangla Finance Ltd. | EGARCH(1,1) | -1.456292 | -0.04154 | 0.775131 | 0.675602 | 0.775131 |

| 17.Meghna Petroleum Ltd. | TGARCH(1,1) | 0.000003 | 0.000203 | 0.999951 | -0.033901 | 0.983203 |

| 18.National Bank Ltd. | TGARCH(1,1) | 0.000050 | 0.449466 | 0.626503 | -0.261835 | 0.945051 |

| 19.National Life Insurance Co. | TGARCH(1,1) | 0.000130 | 0.882162 | 0.490448 | -0.833125 | 0.956047 |

| 20.Olympic Industries Limited | EGARCH(1,1) | -4.818257 | -0.20077 | 0.366885 | 0.278515 | 0.366885 |

| 21.Padma Oil Co.Ltd. | EGARCH(1,1) | -1.519790 | 0.295209 | 0.810922 | 0.678299 | 0.810922 |

| 22.Paramount Textile Limited | EGARCH(1,1) | -2.172623 | 0.005526 | 0.690724 | 1.356606 | 0.690724 |

| 23.Pubali Bank Ltd. | TGARCH(1,1) | 0.000077 | 0.839340 | 0.188616 | -0.057913 | 0.998999 |

| 24.Renata Ltd. | EGARCH(1,1) | -0.774579 | -0.04259 | 0.885217 | 1.172975 | 0.885217 |

| 25.Singer Bangladesh Ltd. | EGARCH(1,1) | -1.22964 | 0.21865 | 0.84335 | 1.12247 | 0.84335 |

Table 3: Continue | ||||||

| 26.Square Pharmaceuticals Ltd. | EGARCH(1,1) | -0.668144 | 0.278965 | 0.906074 | 0.571842 | 0.906074 |

| 27.Summit Power Ltd. | EGARCH(1,1) | -0.441920 | 0.315692 | 0.936363 | 0.645778 | 0.936363 |

| 28.The ACME Laboratories | TGARCH(1,1) | 0.000032 | 0.497928 | 0.657554 | -0.329561 | 0.990702 |

| 29.Titas Gas Trans. & Dist. Co. | EGARCH(1,1) | -1.34786 | 0.24200 | 0.83048 | 0.77380 | 0.83048 |

| 30.United Power Generation | EGARCH(1,1) | -1.86625 | -0.12234 | 0.74437 | 1.21957 | 0.74437 |

Table 4: Appropriate best fitted volatility model for DSE30 companies during Non Covid-19 Periods: 30.04.2019-05.03.2020

| Companies | Model | Persistence | ||||

| 1.Bangladesh Export Import Co. | EGARCH(1,1) | -1.0827 | 0.2579 | 0.8541 | 0.7047 | 0.8541 |

| 2. Bangladesh Steel Re-Rolling | GARCH(1,1) | 0.000007 | 0.0420 | 0.9361 | N/A | 0.9781 |

| 3.Bangladesh Submarine Cab Co. | TGARCH(1,1) | 0.0002 | 0 | 0.6519 | 0.1469 | 0.72535 |

| 4.BBS Cables Limited | EGARCH(1,1) | -0.3632 | -0.0319 | 0.9526 | 0.2371 | 0.9526 |

| 5.Beacon Pharmaceuticals Ltd. | EGARCH(1,1) | -0.0689 | 0.0831 | 0.9874 | 0.2834 | 0.9874 |

| 6.Beximco Pharmaceuticals Ltd. | GARCH(1,1) | 0.000034 | 0.469540 | 0.429895 | N/A | 0.899435 |

| 7.BRAC Bank Ltd. | GARCH(1,1) | 0.000027 | 0.403497 | 0.595503 | N/A | 0.999 |

| 8.British American Tobacco Bangladesh Co | GARCH(1,1) | 0.000035 | 0.471713 | 0.527287 | N/A | 0.999 |

| 9.City Bank Ltd. | GARCH(1,1) | 0.000009 | 0.061663 | 0.918882 | N/A | 0.980545 |

| 10.Confidence Cement Ltd. | TGARCH(1,1) | 0.000000 | 0.000010 | 0.983929 | 0.026449 | 0.997163 |

| 11.Eastern Bank Ltd. | EGARCH(1,1) | -0.138511 | -0.237892 | 0.982994 | -0.120883 | 0.982994 |

| 12.Grameenphone Ltd. | EGARCH(1,1) | -2.656790 | 0.139577 | 0.655068 | 0.736247 | 0.655068 |

| 13.IDLC Finance Limited | EGARCH(1,1) | -0.177014 | -0.080840 | 0.978620 | -0.002799 | 0.978620 |

| 14.IFAD Autos Limited | GARCH(1,1) | 0.000110 | 0.187100 | 0.648693 | N/A | 0.835793 |

| 15.LafargeHolcim Bangladesh | GARCH(1,1) | 0.000041 | 0.483259 | 0.515740 | N/A | 0.998999 |

| 16.Lanka Bangla Finance Ltd. | EGARCH(1,1) | -0.348347 | -0.017496 | 0.951265 | 0.182650 | 0.951265 |

| 17.Meghna Petroleum Ltd. | EGARCH(1,1) | -0.907031 | 0.226582 | 0.890527 | 0.206631 | 0.890527 |

| 18.National Bank Ltd. | TGARCH(1,1) | 0.000002 | 0.019106 | 1.000000 | -0.040489 | 0.998861 |

| 19.National Life Insurance Co. | TGARCH(1,1) | 0.000116 | 0.588382 | 0.547951 | -0.395768 | 0.938449 |

| 20.Olympic Industries Limited | GARCH(1,1) | 0.000023 | 0.180236 | 0.752548 | N/A | 0.932784 |

| 21.Padma Oil Co.Ltd. | EGARCH(1,1) | -0.237036 | 0.097940 | 0.969599 | 0.298089 | 0.969599 |

| 22.Paramount Textile Limited | EGARCH(1,1) | -0.648918 | 0.043452 | 0.915312 | 0.289740 | 0.915312 |

| 23.Pubali Bank Ltd. | TGARCH(1,1) | 0.000002 | 0.010457 | 0.999890 | -0.048330 | 0.986182 |

| 24.Renata Ltd. | EGARCH(1,1) | -1.324554 | 0.111528 | 0.839825 | 1.392414 | 0.839825 |

| 25.Singer Bangladesh Ltd. | EGARCH(1,1) | -1.891748 | -0.104068 | 0.773920 | 0.301164 | 0.773920 |

| 26.Square Pharmaceuticals Ltd. | TGARCH(1,1) | 0.000000 | 0.000000 | 0.964232 | 0.069535 | 0.998999 |

| 27.Summit Power Ltd. | EGARCH(1,1) | -4.19921 | -0.30750 | 0.51996 | 0.69320 | 0.51996 |

| 28.The ACME Laboratories | EGARCH(1,1) | -2.722529 | 0.247366 | 0.674825 | 0.476675 | 0.674825 |

| 29.Titas Gas Trans. & Dist. Co. | EGARCH(1,1) | -0.199619 | 0.286560 | 0.974167 | 0.368539 | 0.974167 |

| 30.United Power Generation | EGARCH(1,1) | -1.976929 | 0.237925 | 0.740295 | 0.576749 | 0.740295 |

The volatility persistence of BRAC Bank Ltd., British American Tobacco Bangladesh, Confidence Cement Ltd., LafargeHolcim Bangladesh, National Bank Ltd., Square Pharmaceuticals Ltd. Companies are extremely high and stationary but volatility persistence value of all companies is less than one.

From the Table 5 and Figure 1 try to see the relative persistence during financial crisis period relative to the overall period. With this result from this Table 5, relative persistence of Summit Power Ltd. during financial crisis is about two times that of the overall period and it has the highest relative persistence. Relative persistence of The ACME Laboratories during financial crisis is about 1.5 times that of the overall period and it has the 2nd highest relative persistence. Relative persistence of Grameen phone Ltd. during financial crisis is about 1.32 times that of the overall period and it has the 3rd highest relative persistence. Relative persistence of Bangladesh Submarine Cab Co. and IFAD Autos Limited during financial crisis is about 1.2 times that of the overall period and it has the 4th highest relative persistence. Relative persistence of Meghna Petroleum Ltd. during financial crisis is about 1.1 times that of the overall period and it has the 5th highest relative persistence.

Relative persistence of Bangladesh Export Import Co., Beximco Pharmaceuticals Ltd., IDLC Finance Limited, National Life Insurance Co., Pubali Bank Ltd., Renata Ltd., Singer Bangladesh Ltd. and United Power Generation during financial crisis is about 1 times higher that of the overall period. And Relative persistence of remaining 14 companies during financial crisis is less than 1 times higher that of the overall period and among 14 companies the Relative persistence of Olympic Industries Limited is lowest during financial crisis relative to overall period.

Table 5: Relative Persistence between COVID -19 Period and non COVID -19 Period

| Companies | Persistence during COVID -19 Period | Persistence during non COVID -19 period | Relative Persistence |

| Bangladesh Export Import Co. | 0.92 | 0.85 | 1.07 |

| Bangladesh Steel Re-Rolling | 0.93 | 0.98 | 0.95 |

| Bangladesh Submarine Cab Co. | 0.87 | 0.73 | 1.20 |

| BBS Cables Limited | 0.90 | 0.95 | 0.95 |

| Beacon Pharmaceuticals Ltd. | 0.81 | 0.99 | 0.82 |

| Beximco Pharmaceuticals Ltd. | 0.96 | 0.90 | 1.07 |

| BRAC Bank Ltd. | 0.82 | 1.00 | 0.82 |

| British American Tobacco Bangladesh Co | 0.70 | 1.00 | 0.70 |

| City Bank Ltd. | 0.96 | 0.98 | 0.98 |

| Confidence Cement Ltd. | 0.86 | 1.00 | 0.86 |

| Eastern Bank Ltd. | 0.88 | 0.98 | 0.90 |

| Grameenphone Ltd. | 0.86 | 0.66 | 1.32 |

| IDLC Finance Limited | 1.00 | 0.98 | 1.02 |

| IFAD Autos Limited | 1.00 | 0.84 | 1.20 |

| LafargeHolcim Bangladesh | 0.87 | 1.00 | 0.87 |

| Lanka Bangla Finance Ltd. | 0.78 | 0.95 | 0.81 |

| Meghna Petroleum Ltd. | 0.98 | 0.89 | 1.10 |

| National Bank Ltd. | 0.95 | 1.00 | 0.95 |

| National Life Insurance Co. | 0.96 | 0.94 | 1.02 |

| Olympic Industries Limited | 0.37 | 0.93 | 0.39 |

| Padma Oil Co.Ltd. | 0.81 | 0.97 | 0.84 |

| Paramount Textile Limited | 0.69 | 0.92 | 0.75 |

| Pubali Bank Ltd. | 1.00 | 0.99 | 1.01 |

| Renata Ltd. | 0.89 | 0.84 | 1.05 |

| Singer Bangladesh Ltd. | 0.84 | 0.77 | 1.09 |

| Square Pharmaceuticals Ltd. | 0.91 | 1.00 | 0.91 |

| Summit Power Ltd. | 0.94 | 0.52 | 1.80 |

| The ACME Laboratories | 0.99 | 0.67 | 1.47 |

| Titas Gas Trans. & Dist. Co. | 0.83 | 0.97 | 0.85 |

| United Power Generation | 0.74 | 0.74 | 1.01 |

Observing that mean returns of DSE30 companies are not zero between two periods except singer Bangladesh Ltd. of Covid-19 period while median of Covid-19 period are all about zero but with regards to overall periods medians are non zero except Eastern Bank Ltd., National Bank Ltd., Public Bank Ltd. and Summit power Ltd. The standard deviations of covid-19 period are higher than overall periods indicating high variability around the mean across DSE30 companies. So concluding that variation of DSE30 companies for covid-19 period is high than overall

From Table 3, clear to us that there is no DSE30 companies are fitted with ARCH(1), only Beximco Pharmaceuticals Ltd. is fitted with GARCH(1,1) and remaining 21 companies i.e. Bangladesh Export Import Co., Bangladesh Steel Re-Rolling, Bangladesh Submarine Cab Co., Beacon Pharmaceuticals Ltd., BRAC Bank Ltd., British American Tobacco Bangladesh Co., Confidence Cement Ltd., Eastern Bank Ltd., Grameenphone Ltd., IFAD Autos Limited, Lafarge Holcim Bangladesh, Lanka Bangla

Finance Ltd., Olympic Industries Limited, Padma Oil Co.Ltd., Paramount Textile Limited, Renata Ltd., Singer Bangladesh Ltd., Square Pharmaceuticals Ltd., Summit Power Ltd., Titas Gas Trans. & Dist. Co., United Power Generation companies are fitted with EGARCH(1,1), and also remaining 9 companies i.e BBS Cables Limited, City Bank Ltd., IDLC Finance Limited, Meghna Petroleum Ltd., National Bank Ltd., National Life Insurance Co., Public Bank Ltd., The ACME Laboratories are fitted with TGARCH(1,1) models.

The volatility persistence of IDLC Finance Limited, IFAD Autos Limited, Public Bank Limited, The ACME Laboratories companies are extremely high and stationary. So according to result say that DSE30 companies of financial crisis periods produces instability in the capital market, destabilizes the value of currency, as well as hampers international trade and finance.

From Table 4, clear to us that there is no DSE30 companies are fitted with ARCH(1) and 8 companies such as Bangladesh Steel Re-Rolling, Beximco Pharmaceuticals Ltd., BRAC Bank Ltd., British American Tobacco Bangladesh Co., City Bank Ltd., IFAD Autos Limited, Lanka Bangla Finance Ltd, Olympic Industries Limited companies are fitted with GARCH(1,1) and 16 companies such as Bangladesh Export Import Co., BBS Cables Limited, Beacon Pharmaceuticals Ltd., Eastern Bank Ltd., Grameenphone Ltd., IDLC Finance Limited, Lanka Bangla Finance Ltd., Meghna Petroleum Ltd., Padma Oil Co.Ltd., Paramount Textile Limited, Renata Ltd., Singer Bangladesh Ltd., Summit Power Ltd., The ACME Laboratories, Titas Gas Trans. & Dist. Co., United Power Generation companies are fitted with EGARCH(1,1) and remaining 6 companies such as Bangladesh Submarine Cab Co., Confidence Cement Ltd., National Bank Ltd., National Life Insurance Co., Pubali Bank Ltd., Square Pharmaceuticals Ltd. companies are fitted with TGARCH(1,1) models.

The volatility persistence of BRAC Bank Ltd., British American Tobacco Bangladesh, Confidence Cement Ltd., LafargeHolcim Bangladesh, National Bank Ltd., Square Pharmaceuticals Ltd. Companies are extremely high and unstationary but volatility persistence value of all companies is less than one.

With this result from this Table 5, relative persistence of Summit Power Ltd. during financial crisis is about two times that of the overall period and it has the highest relative persistence. Relative persistence of The ACME Laboratories during financial crisis is about 1.5 times that of the overall period and it has the 2nd highest relative persistence. Relative persistence of Grameen phone Ltd. during financial crisis is about 1.32 times that of the overall period and it has the 3rd highest relative persistence. Relative persistence of Bangladesh Submarine Cab Co. and IFAD Autos Limited during financial crisis is about 1.2 times that of the overall period and it has the 4th highest relative persistence. Relative persistence of Meghna Petroleum Ltd. during financial crisis is about 1.1 times that of the overall period and it has the 5th highest relative persistence. Remaining among 14 companies the Relative persistence of Olympic Industries Limited is lowest during financial crisis relative to overall period.

Banamber, M and Matiur, R. "Dynamics of stock market return volatility: Evidence from the daily data of India and Japan." International Business & Economics Research Journal vol. 9, no. 5, 2010, https://doi.org/ 10.19030/I ber.v9i5.571.

Debesh, B. "Stock market volatility: An evaluation." International Journal of Scientific and Research Publications vol. 3, no. 10, 2013, ISSN 2250-3153.

Mamtha, D and Sakthi Srinivasan K. "Stock market volatility - conceptual perspective through literature survey." Mediterranean Journal of Social Sciences vol. 7, no. 1, 2016, https://doi.org/10.5901/mjss.2016.v7n1p208.

Maqsood, A et al. "Modeling stock market volatility using GARCH models: A case study of Nairobi Securities Exchange (NSE)." Open Journal of Statistics vol. 7, 2017, pp. 369–381. https://doi.org/10.4236/ojs.2017.72026.

Raheem, M.A and Samson, T.K. "Volatility modelling of global financial crises effects on the Nigerian banks." Open Journal of Statistics vol. 10, no. 2, 2020, pp. 303–324. https://doi.org/10.4236/ojs.2020.102021.Reference 1

Roni, B and Shouyang, W. "Stock market volatility and return analysis: A systematic literature review." Entropy vol. 22, 2020, https://doi.org/10.3390/e22050522.

Sartaj, H et al. "Stock market volatility: A review of the empirical literature." IUJ Journal of Management vol. 7, no. 1, 2019, https://doi.org/10.11224/IUJ.07.01.15.